August 19, 2013

August 19, 2013 4 min

4 min Written by: Arian Borys, Licensed Insurance Broker (Level 3), Humberview Insurance Brokers

Written by: Arian Borys, Licensed Insurance Broker (Level 3), Humberview Insurance Brokers Understanding Insurance Valuations vs Property Purchase Price

A frequent inquiry in insurance discussions involves the disparity between the insurance coverage amount and the property’s purchase price. Clients often wonder, “Why is the building coverage valued at $385,000 when I purchased the property, including the land, for just $265,000?” This question is both valid and common, and to address it, we’ll provide both a concise and a detailed explanation.

The Short Explanation

Simply put, the purchase price of your property and the cost to rebuild it in the event of a total loss are two distinct concepts. For instance, consider a home in Oshawa that might cost $200,000 to buy but would require $400,000 to rebuild after a total loss. Property values for Oshawa homes are typically lower than Etobicoke homes. However, building the same house in Etobicoke would cost nearly $400,000, while its market price could exceed $700,000.

The Detailed Explanation

The market value of your home – the price a buyer is willing to pay – doesn’t influence your home insurance value. Insurance brokers use specialized evaluation programs to estimate the insurable value of your home, focusing on the cost to rebuild it in today’s market. Several factors play into this calculation:

- Current Material Costs: If your house was constructed 50 years ago, rebuilding costs are higher now due to inflation affecting material prices.

- Labour Costs: Similarly, the cost of labour has increased over time. What was affordable 50 years ago is more expensive now.

- Demolition and Debris Removal: This includes the expense of dismantling damaged structures and clearing debris.

- Increased Material Costs in Isolated Construction: Original construction often occurs in bulk, with developers enjoying discounted rates for materials. Rebuilding a single home today incurs higher per-unit material costs.

- Elevated Labour Costs in Individual Projects: Large-scale developments often secure more favorable rates from subcontractors. When rebuilding a single house, these cost advantages don’t apply.

while the market value of your property and its insured value may differ significantly, the latter is calculated to ensure your home’s complete and current reconstruction value is covered.

Deciphering Co-Insurance and Its Impact on Insuring Below Property Valuation

Clients often inquire about the possibility of insuring their property for less than its evaluated value, typically motivated by the desire to reduce insurance premiums. While our recommendation is always to insure up to 100% of the property’s valuation, there are scenarios where insuring for less is feasible without incurring penalties. This is especially relevant in the context of commercial insurance policies, which often include a co-insurance clause.

Understanding Co-Insurance Clauses

A co-insurance clause in an insurance policy specifies a minimum percentage of the property’s evaluated value for which it must be insured. This percentage typically ranges from 80% to 100%. For example, if a policy features an 80% co-insurance clause, the policyholder is permitted to insure the property for just 80% of its assessed value without facing penalties. For instance, a property evaluated at $100,000 can be insured for $80,000, and in the event of a total loss, the policyholder would receive $80,000.

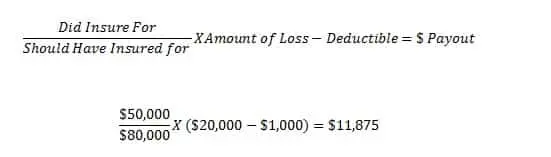

Consequences of Placing Building Insurance Below the Co-Insurance Value

Opting to insure a property for less than its co-insurance value can lead to substantial penalties in cases of partial losses. Consider a property with a $100,000 rebuilding cost and an 80% co-insurance clause. If the owner chooses to insure it for only $50,000, they would indeed receive $50,000 in the event of a total loss. However, in the event of a partial loss – say, damages amounting to $20,000 with a $1,000 deductible – the co-insurance penalty comes into play. This penalty is calculated as follows:

Because you insured for only 62.5% of what you should have insured the building for ($80,000) you will be penalized in the event of a partial loss and only receive a partial amount of the claim. Which is why we always recommend to insure to 100% of the evaluation. This is why when getting quotes on home insurance or property insurance to always check the building values on the quotation. Lately, few companies will even allow insuring for less than the evaluation of a property in any case.

Determining the Appropriate Insurance Coverage

Deciding the right insurance coverage for your property is ultimately your decision, but it’s best approached with informed guidance. Engaging a reputable property inspection company for a thorough property appraisal is highly recommended. A professional appraisal will assess your house or building accurately, providing you with an up-to-date replacement cost. This figure reflects what it would cost to rebuild your property in today’s market, ensuring that your insurance coverage aligns with current values and minimizes financial risks in unforeseen events. Remember, insurance brokers are not usually qualified to conduct accurate building appraisals, and any appraisals done by an insurance broker are more of a guideline then anything.